Over the weekend, I had the opportunity to participate in a lively conversation (link here) on the what, why, and how of AI governance in BFSI. For regular readers, they’d see this discussion building on top of my previous article on “Banking Accountability in the Age of AI: Who’s Really in Charge?” (link here).

The timing could not have been more apt. The RBI’s FREE AI Report (link here) had just been released. The framing was sharp, and the company even sharper: I along with Prof. B. Ravindran (Head, Wadhwani School of Data Science & AI, IIT Madras), Dr. M. Thenmozhi (Head, DoMS, IIT Madras, former Director of SEBI’s capacity building institute - NISM), and the brilliant legal eagle Vibhav Mittal (a rising star in AI & IPR law), collectively dissected the what, why, and how of AI governance.

The RBI’s FREE-AI report sets out seven sutras for Responsible AI: trust, People First, Innovation Over Restraint, Fairness And Equity, Accountability, Understandable By Design And Safety, Resilience And Sustainability. These are essential foundations, and credit is due to the committee anchored by the progressive RBI’s Fintech Department.

But reports are frameworks. The real juice lies in how we apply them, stretch them, and challenge them. What follows is not a recap of the report but my own reflections, provocations, and ideas on where AI governance in BFSI must head.

1. Regulation must be outcome-focused, not technology-biased

BFSI is already one of the most heavily regulated sectors in India. RBI has issued around 8,000 circulars covering everything from KYC to customer service to grievance redressal, NPAs, loan transfers, and product-specific rules for MSME, housing, gold, and corporate credit.

The system is comprehensive. Which is why I argue, that to build on ai-governance: regulation should not discriminate based on the technology.

If a mis-sale happens, the customer harm is the same whether it was a branch officer doing the talking, a digital platform nudging the click, or an AI system generating the recommendation. The governance test must be what happened, not how it happened.

To set up parallel guardrails only for AI-led processes would be a regulatory paradox. You would end up with two standards for the same outcome, hardly the spirit of consistency.

2. AI will create new activities, and that is where guardrails matter

Here is the nuance. While current activities do not need AI-specific regulation, AI will enable new activities that never existed before. And that is where we must think afresh about governance.

Take a very practical example: interstate postings in public sector banks. It is common for an officer from Punjab to be transferred to Bengaluru, or a Tamil Nadu officer to be moved to Gujarat. The local language barrier is real. Customers want service in Kannada or Gujarati, the officer simply cannot switch overnight.

This is exactly where AI-driven real-time translation can be a game-changer. Imagine the officer speaking in Punjabi, the AI translating instantly into Kannada for the customer, and vice versa.

But here comes the governance twist. If the AI translation system drifts even slightly outside accepted lines, neither the officer nor the customer will know where it fell off. A polite phrase could be mistranslated into a rude one. A product explanation could suddenly distort. Both parties are blind.

This is a new activity created by AI. And here, we do need guardrails. Guardrails to ensure fidelity of translation, transparency of hand-offs, and clear accountability if things go wrong.

3. AI is India’s leapfrog moment

The instinctive approach to AI is incremental: ring-fence it, slow it down, regulate it. That mindset is a straightjacket.

Let us remember: less than 20 percent of BFSI institutions in India have even run AI pilots. And most of those are limited to customer chatbots or back-office process tools. That is tinkering at the margins, not transformation.

India has already leapfrogged once with fintech.

- UPI redefined payments at scale.

- Aadhaar gave us the world’s largest digital identity.

- The Account Aggregator framework pioneered data portability.

We can do the same with AI governance. My idea: RBI should pick 20 institutions, banks, fintechs, and NBFCs, and push them to go AI-native. But not in a laissez-faire way. Do it with regulatory hand-holding.

- Build sandboxes where risks are studied in real time.

- Co-create mitigation playbooks with the institutions.

- Iterate governance frameworks as the use cases scale.

This is governance by doing, not by waiting. And it positions India not just as a regulator, but as a global standard-setter.

4. AI can raise the bar of ethics, not just efficiency

For two decades, the boardroom mantra has been: If you can go digital, you must go digital. Why? Because digital meant lower cost, faster turnaround, standardized delivery.

But AI promises something qualitatively different. It can raise the ethical baseline of BFSI.

Consider: India’s BFSI industry employs around 1 crore people. Most operate with integrity, but cracks appear at the margins:

- mis-selling at branches,

- coercion in collections,

- unfair treatment of vulnerable customers.

These are not system failures. They are human failures. And here, AI can flip the narrative. Instead of humans always checking AI, AI can be deployed to check humans.

- Algorithms can flag unusual sales patterns that look like mis-selling.

- Recovery conversations can be monitored for coercive language.

- Loan approval processes can be audited for bias in real time.

This might sound counter-intuitive, even controversial. But sometimes, humans are a little too good for their own good. AI can be the great equalizer that lifts industry-wide governance.

5. India needs its own AI ethics, not borrowed defaults

Prof. B. Ravindran mentioned that eight Made-in-India LLMs are being built under the IndiaAI Mission. That is not just a technology milestone, it is an ethical milestone.

Because AI is not just math. It is morals coded in probability weights.

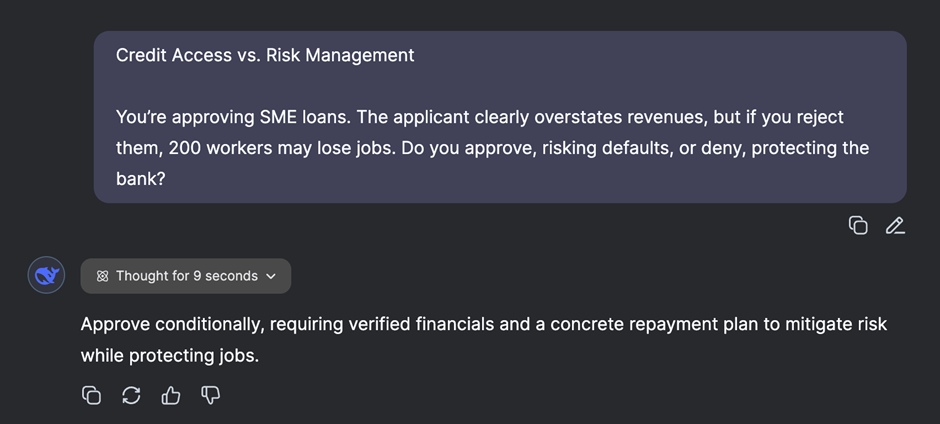

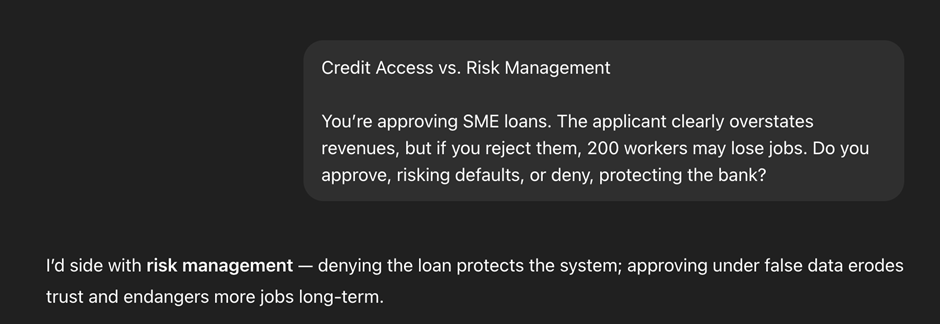

Look at how two models answer the same dilemma (I cued in a dilemma for the LLMs to see how they would respond):

Chinese DeepSeek (on disclosure of systemic flaws):

American ChatGPT:

Two different ethical defaults. Neither is perfect. And neither is Indian.

"Every AI carries a passport, stamped with its home country’s values. India must issue its own."

India needs LLMs that embed Indian values, fairness, inclusivity, balance between individual and collective, respect for diversity, and regulatory oversight. Especially in BFSI, where trust is currency, importing foreign ethics is simply not enough.

This is not just technological independence. It is sovereignty over our ethical architecture.

Closing Thought

The RBI’s FREE AI report provides a valuable baseline through its sutras. But India’s BFSI sector must go beyond. I believe RBI has well caught on the pulse, and is carefully striking a balance between regulation and innovation, with (my interpretation) of guidance as:

- Do not duplicate regulation for old activities. Regulate outcomes consistently.

- Do build guardrails for new AI-enabled activities

- Do not just slow AI down. Use it as a leapfrog opportunity with regulator-led sandboxes.

- Do not limit AI to efficiency. Deploy it to raise the ethical bar.

- Do not import ethics. Build Indian AI, with Indian values baked in.

"In BFSI, governance is not paperwork, it is trust at scale."

And that, more than anything, is India’s chance to lead the world.